The first ethical funds for UK retail investors were pioneered in the early 1980s, and since then client demand for responsible investment has increased tremendously.

The field has since moved from the fringes of the industry to a strategic priority for many asset managers not wanting to miss out on market share.

The industry has responded with numerous new fund launches to capture the inflows and we have seen the Investment Association discuss setting up new environmental, social and governance sector categories.

ESG is a regulatory priority for advisers too, after the European Commission’s Delegated Regulation (EU) 2017/565 – which suggest that advisers now need to incorporate clients’ ESG preferences into the scope of suitability considerations.

Investors can now choose from a number of active and passive funds that deploy some sort of responsible investing technique.

Some exclude ‘harmful’ or ‘unethical’ business practices or industries from portfolios. Many invest only in businesses that contribute positively to the planet or to society. Others will invest in companies with poor practices to improve their behaviour.

There is, unfortunately, little consistency across the fund groups.

The moral argument for these strategies is strong, but does doing good reduce or add to future returns? Nobel Prize-winning economist Harry Markowitz’s modern portfolio theory would suggest that if an investor reduces their investment opportunity set, then their odds of adding value decreases.

Put another way, a screened portfolio would perform worse than an unscreened one. Some investors are candid about this; Norway’s sovereign wealth fund discloses publicly what it believes has been the opportunity cost to returns of investing ethically since 2006.

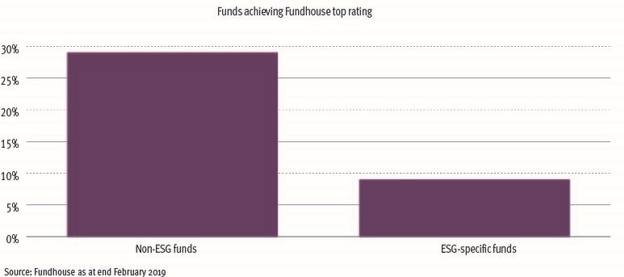

We also find, more broadly, that these funds do struggle to perform, in aggregate, relative to funds with no constraint, as shown in the chart below.

But there are caveats to these findings. Academic evidence, for example, suggests that improving governance in companies (the ‘G’ in ‘ESG’) will be additive to investment returns. Managers become better custodians of shareholder capital and this drives better return on capital.

Others highlight the financial benefits of needing a very long-term view, where investing in a promising renewable energy technology, for example, will likely pay as it becomes mainstream.

Or perhaps avoiding investing in companies with high carbon footprints that are highly profitable in the near-term but may be hit by carbon taxes or customer revolt in future. However, evidence for these benefits is mixed.

There is also confusion with terminology used to describe these funds.

Terms like ‘socially responsible’, ‘impact’ and ‘ethical’ mean different things to different people.

And this manifests itself in funds with the same ESG labels having opposing views. Why does this fund hold Alphabet while this one screens it out? Why do some own the most responsible alcohol producers, when others rule them all out? It is confusing.

There is also the question of value for money. So few fund managers of ESG strategies see excess returns as a priority, preferring to focus their ‘value add’ on the ESG side.